The ripple effects of ZIRP

I made some notes for myself to trace the effects of the Zero Interest Rate Policy (ZIRP) adopted by the US Federal Reserve in Mar 2020. There's also a tweet thread here that covers ZIRP's effects on India Tech hiring.

ZIRP as a response to the Covid outbreak

The Covid outbreak caused a sharp slowdown in the world economy due to several inter-connected factors playing out all at once.

The lockdown kicked in and people were stuck at home - resulting in offline businesses taking a hit. Consumers became fearful and spent less. Businesses had to cut back on marketing and hiring - in anticipation of low sales. Supply chain routes were affected. Restaurants and Malls closed down. Discretionary spending was down.

The Federal Reserve had to act quick in order to avoid permanent damage in the form of US businesses having to shut down, loan defaults, spike in unemployment rates, increase in large institutions requiring bailouts, angst against the current government, higher crime rates, etc.

Slashing interest rates was one way to avoid the pain. Because low interest rates, i.e. a ZIRP (Zero Interest Rate Policy) is meant to kickstart an economy from a recession.

What does it mean for the Fed to "slash interest rates?"

When the economy is heating up and there is too much action (i.e. inflation), the Fed raises interest rates. On the other hand if the economy is down, the Fed slashes rates.

But what does it mean to "slash interest rates"?

A group of Fed officials meet 8 times in a year to decide what the "Interest Rate On Reserve Balances" will be. This is the interest rate they decided to keep close to 0 and what we call as the Zero Interest Rate Policy.

To understand how "Interest on Reserve Balances" work, let's take a step back.

Retail banks in the USA deposit some of their cash balance with the Federal Reserve. And the Fed, in turn, decides how much interest to pay to the retail banks for their deposit.

Apart from depositing it with the Fed, Retail banks also deposit their cash with other fellow retail banks. And the "Interest Rate on Reserve Balances" set by the Fed goes on to influence the interest rates that retail banks charge each other to keep their deposits with each other.

When the "Interest Rate on Reserve Balances" is close to 0, it becomes unappealing for retail banks to hold reserves with each other or the Fed. These retail banks would much rather loan the cash out to their customers at some rate that's higher than 0% to make some money at least.

The way banks increase the amount of loans they give out is by slashing consumer loan rates so it becomes more appealing for bank customers to take, for example, mortgages. So we see how slashing the Fed Funds rate also reduces home loan mortgage rates, boosting housing market.

Pulling this "Interest Rate on Reserve Balances" lever has a ripple effect on various other interest rates too - such as the credit card rates, business loan rates, savings deposit rates and so on.

These ripple effects are large and somewhat predictable at least for the 2nd and 3rd degree effects. Which gives the Fed power to influence the US, and in turn, the worldwide economy (i.e. at some point downstream, it affects Indian software engineer salaries too, which is more like a 6th degree effect.)

Slashing Interest Rates improves Spending, by lowering the cost of Borrowing

Let's take an example. If a bank calls you and offers you a 30 year home loan goes down to as low as 2.6% interest rates, you are going to seriously consider purchasing a house. You'd likely stretch your budgets too, beyond your means, to buy a house as large as possible. That's because at a 2.6% interest rate, borrowing is cheap.

Now imagine several 100s of thousands of people borrowed to purchase or invest because it was cheap to do so, this injects cash back into the economy, kickstarting it and bringing a country out of recession. (Well, out of recession and into inflation but that's a separate topic.)

That's exactly what happened. Home loans dropped to ~2.6% back in mid 2020 when the Fed slashed interest rates. Whereas normally it would be ~5-7%.

The reason home loan interest rates, along with various other types of interest rates, dropped that drastically in early 2020 is because the Federal Reserve decided to adopt ZIRP.

Slashing Interest Rates also makes investors more willing to take on larger risks to get higher returns

The Fed slashing interest rates influenced the risk/reward tradeoffs for investors. To understand how this plays out, let's start with how Treasure Bills work.

Treasure Bills (or T-Bills) are bonds that are issued by the US government that you can invest in.

By buying T-Bills you are effectively lending to the US government. And the government pays you an "interest" for borrowing from you. The defining feature of investing in T-Bills is that it's risk free, since the US government is unlikely to default.

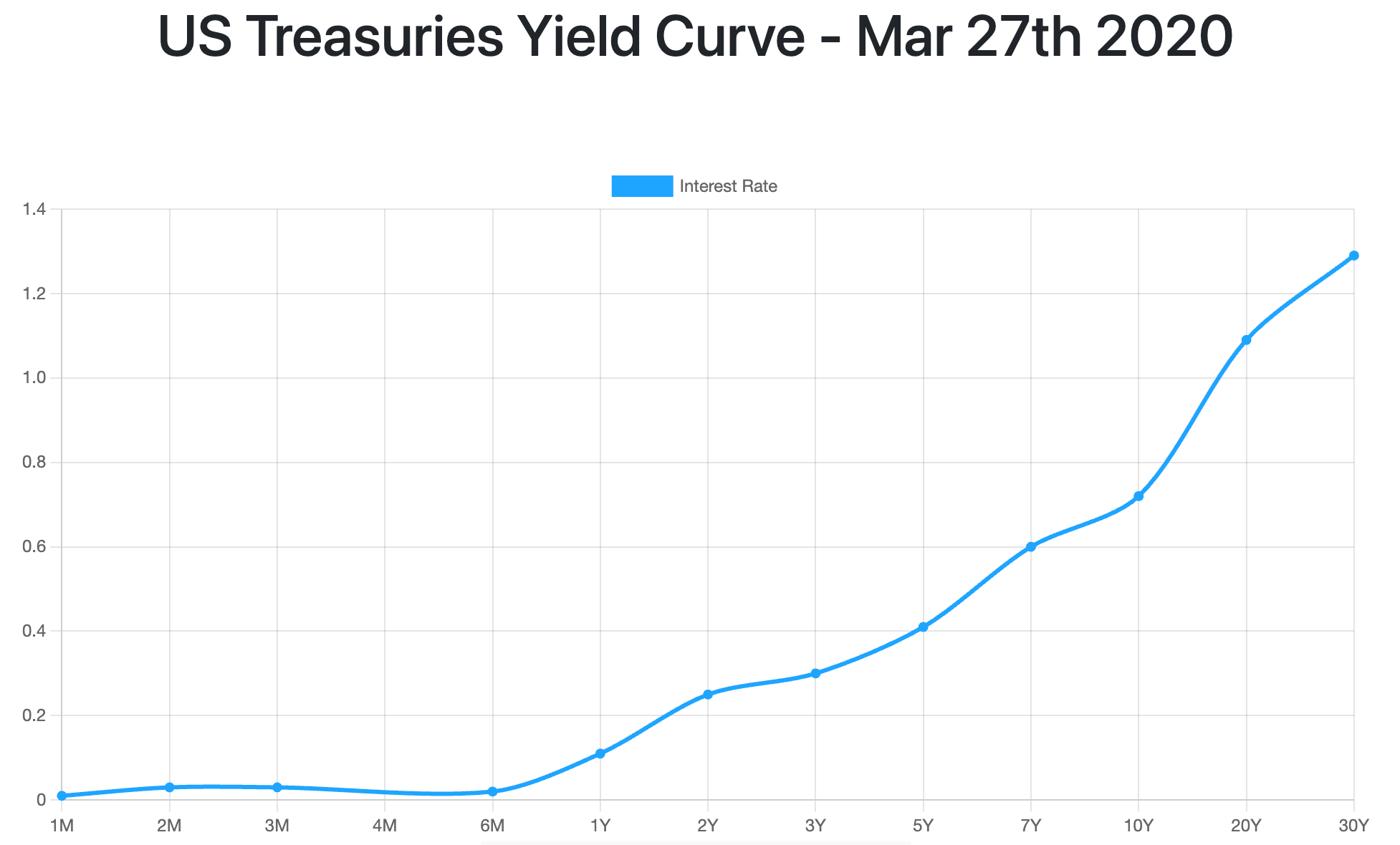

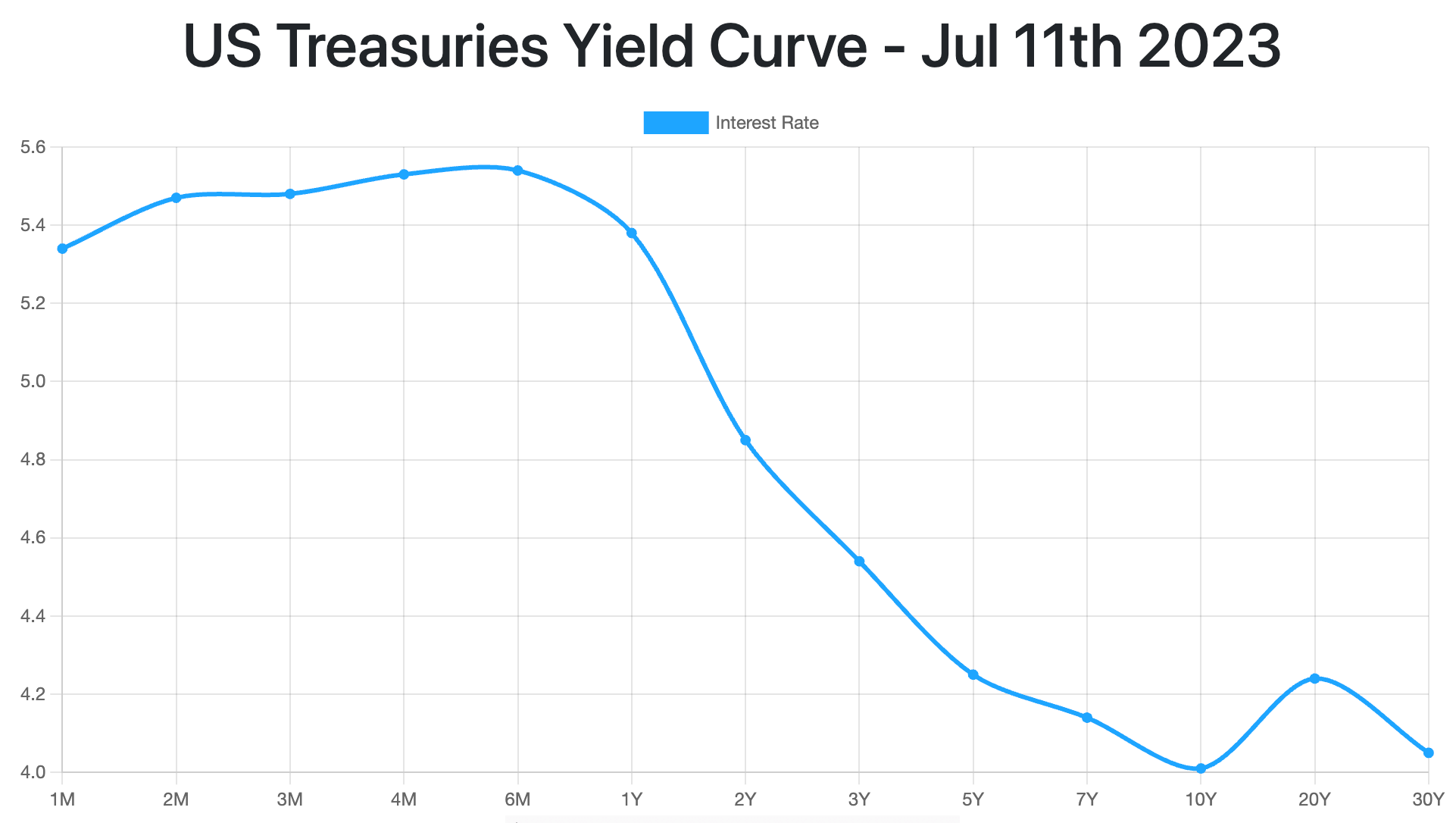

In a weak and uncertain economy, which was the case in Mar 2020, investors flock to safer investments like T-Bills. This drives down yields because of the large demand for T-Bills.

The above 2 charts highlight how T-Bill yields dropped sharply as a result of ZIRP.

In Mar 27th 2020, the yield on the 1 month T-Bill was 0.01%. And the yield on the 10Y was a mere 0.75%. This was a direct result of the Fed implementing the Zero Interest Rate Policy in March 2020.

The low yields made investing in safe, government bonds unattractive. And investors (think large institutional investors) started looking at higher risk opportunities such as investing in Venture Capital firms.

VC firms then invested in technology companies where one waits for close to a decade to see returns. But the returns themselves are far more lucrative than investing in low returns T-bills.

It helped that technology companies have a reputation of being the future and where all the yield action is.

A decent chunk of this money ended up in the Indian Tech Startup scene. I've made a tweet thread around that here.